Critical Illness Insurance

What it does

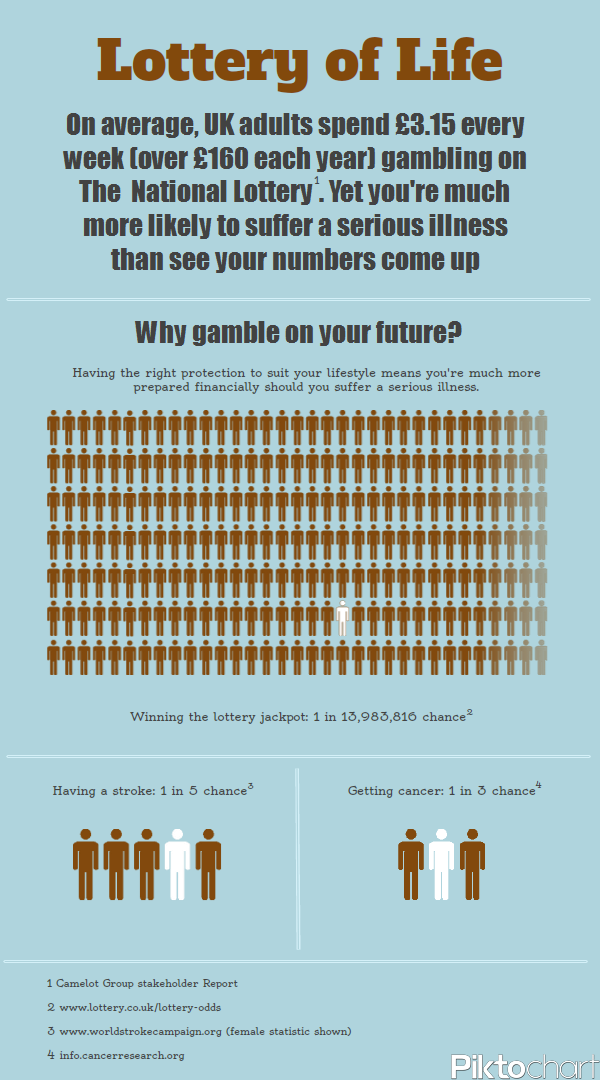

Critical illness insurance pays out a tax-free lump sum on the diagnosis of certain life-threatening or debilitating (but not fatal) conditions including heat attack, stroke, cancer, and major organ transplants. This list will vary depending on the insurer, as will the exclusions for making a claim.

Critical illness often comes as an optional addition to a life insurance policy, but can also be purchased on its own. Policies usually only pay out once, so they don't necessarily replace your regular income, but you can use the money towards medical treatment, your mortgage or anything else you choose.

Why you might need it

Many people buy critical illness insurance when they take on a major commitment, like a mortgage, or start a family. However, since we'd all like to have our financial commitments lightened if we were to suffer a serious illness or injury, the cover is relevant for most of us at any time.

Replacing an existing critical illness policy

If you already have critical illness insurance you should think carefully before you cancel your existing policy and take our a new one.

For example, if you've developed any illnesses since you first took out the policy, you may lose some of the benefits when you replace it. That's because pre-existing medical conditions may not be covered by the new policy.

Recent advances in the treatment of certain conditions, such as cancer, may also have an effect, as a new policy might be more restrictive than an older policy when it comes to paying claims for certain conditions.

A good financial adviser should be able to quickly identify the issues and help you make the right decision about your critical illness insurance.

No comments:

Post a Comment